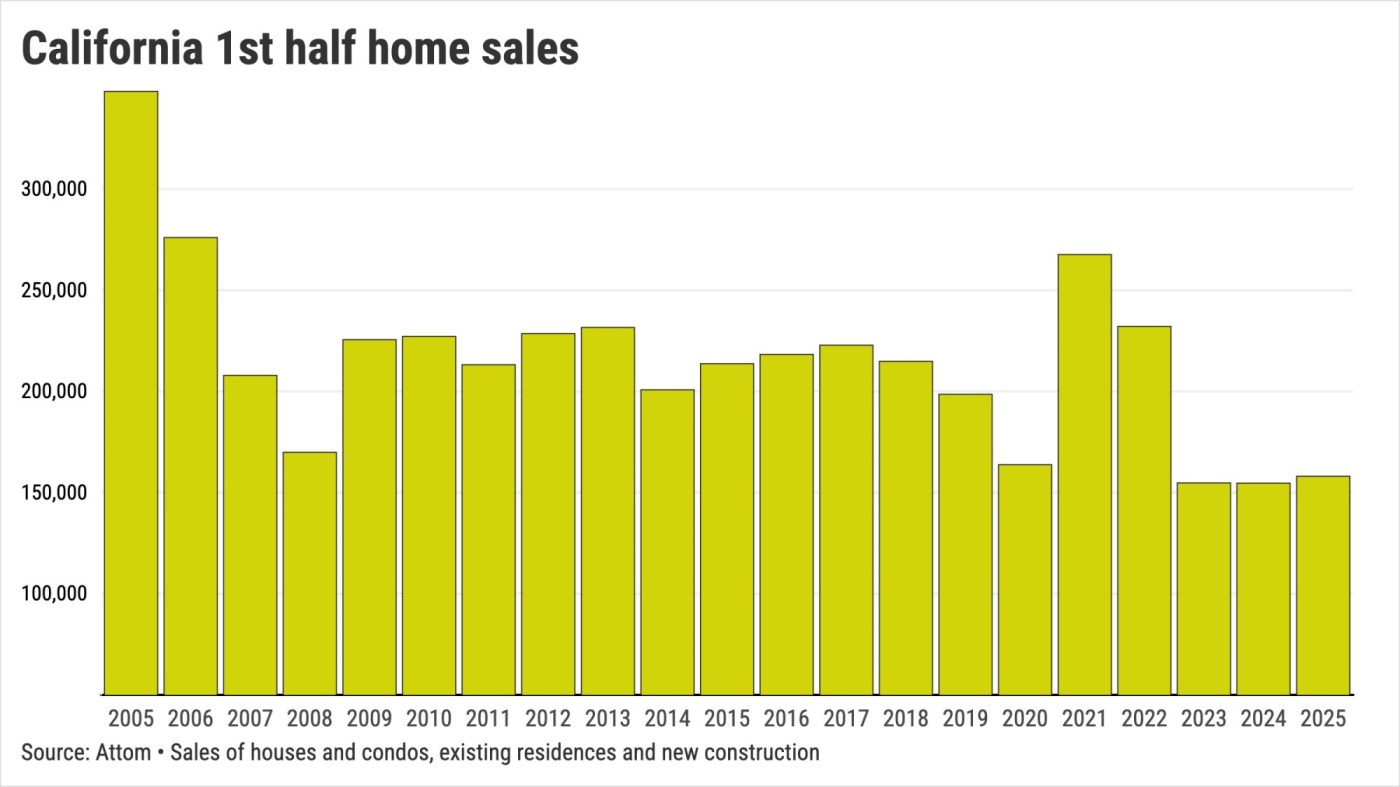

In the first half of 2008, as the global financial system was crashing, 169,946 homes were sold across California.

In 2025’s first six months, only 158,086 residences were bought — 7% below real estate’s ugliest era.

Related Articles

Bay Area home sales dropped in July, but so far prices haven’t followed

Student housing proposed at former San Jose restaurant site

Mayor Barbara Lee has a new plan for solving homeless crisis in Oakland — and it has major financial backing

Does this small city have the Bay Area’s worst homelessness problem?

Future housing levels remain sticking point for Hilltop Mall plans

This is a stark reminder, courtesy of my trusty spreadsheet, of the depths of the recent homebuying collapse. Using sales data from Attom it studied a broad swath of closed transactions, including houses and condos, both existing residences and newly constructed.

Consider how the pandemic era has altered homebuying by examining some simple math: ranking first-half sales since 2005.

California in 2024 had its lowest sales count to start any year. The second-slowest start was 2023. This year was the third-slowest, with 2020 at No. 4.

And bubble-bursting 2008? No. 5.

Let’s politely say the housing market is historically chilled.

The price is wrong

California house hunters remain hesitant because prices remain stubbornly high.

June’s $755,000 median selling price was an all-time high after gaining 6% in three turbulent years. That price gain is a decided cooling from the 39% jump between 2019 and 2022.

But it’s worth noting that prices slipped 26% in the three years before 2008’s debacle. Don’t overlook the role of those mid-crash discounts in spurring that era’s homebuying rebound.

Sales jumped 33% in the next 12 months, ending in June 2009.

Who can afford it?

What’s up with this slump? Well, it’s what’s down: The number of people who can pay up for a home.

The statewide affordability index from the California Association of Realtors tells us that only 15% of households can theoretically qualify to buy a single-family home.

That’s down from 16% three years ago, when mortgage rates were surging off their historic lows. Cheap money overheated real estate and the overall economy.

It’s also down from 23% at mid-year 2021 when home loans were still below 4% compared to 2025’s near 7% financing costs.

And the latest reading is also less than mid-year 2008, when 26% of Californians could theoretically purchase a home.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at [email protected]